Sinking Fund, Lost Opportunity: The Hidden Cost of Paying Cash

By

/ Published:

/ Updated:

/ Read Time:

In Brief:

Paying cash with a sinking fund avoids a loan payment, but it does not eliminate the cost of the purchase. Every dollar spent stops compounding forever. The Infinite Banking Concept uses policy loans to preserve compound growth — so the underlying capital keeps working even while it’s deployed.

In This Article

- The sinking fund argument — and why it’s only half true

- Why paying cash still changes your cash flow

- The opportunity cost of spending money you’ve already saved

- How IBC financing does multiple jobs at once

- What happens to your policy loan when you die

The Common Objection to IBC

One response I have encountered multiple times — and one I held myself when I was first exposed to the Infinite Banking Concept — is that by using the sinking fund method you avoid a monthly payment, while with IBC you still have one.

This is only a half-truth. And it represents the change in thinking required to practice the Infinite Banking Concept and the necessity of thinking long range.

Three Ways to Buy a $30,000 Car

In the article Who Controls the Banking Function (the banking function: storage, movement, and repayment of money), I used the example of purchasing a $30,000 car and showed that you have three options:

- Option A — Pay cash (sinking fund): Spend $30,000 now and give up $4,800 in earnings over five years.

- Option B — Finance with a bank loan: Make monthly installments totaling $34,800, principal and interest to someone else’s bank.

- Option C — Finance with your own banking system (IBC): Make monthly installments totaling $34,800 to your own bank.

In all three cases you are spending $34,800 over the first five years. You will spend $34,800 over those those 5 years no matter what. And I showed the difference in outcome from the three options – and the result of controlling the banking function yourself.

Paying Cash Still Changes Your Cash Flow

Yes — if you choose Option A, you have not signed a loan agreement. You do not have a required monthly loan payment. But it is not accurate to say your cash flow is unchanged.

No matter which option you choose, a banker is involved — either you or someone else. If you choose to be the banker, whether practicing IBC or using the sinking fund, you must be an honest banker.

You cannot take $30,000 from your sinking fund, leave your savings account empty, and expect the money to be there for the next purchase. You must replenish it — and account for time value and inflation as you do.

If you have $30,000 in savings, spend it all on a car, and make no further contributions, you will have $0 when the next car purchase comes. To save $30,000, you need to set aside roughly $470 per month with a conservative 3% APY. To replace the same car adjusted for inflation, you need to set aside $545 per month.

Whether you are making a loan repayment or replenishing a savings account, future cash flow is required — and it must increase over time.

The sinking fund, like IBC, does not have a required monthly payment. But like IBC, you would be foolish to have no repayment plan.

The Hidden Cost: Opportunity Lost

Here is where the sinking fund method falls significantly short.

When you spend $30,000 from savings, those dollars stop working for you permanently. Like an employee you have let go, they will never produce for you again.

- Untouched, that $30,000 could have earned $4,800 in the first five years. And then more after.

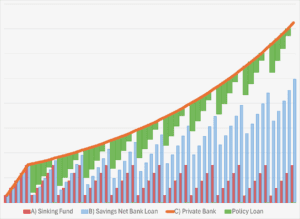

- Over 55 years, that same $30,000 could have compounded to over $155,000.

In an effort to avoid paying $4,800 in interest to someone else’s bank (Option B) — or even $3,600 to your own bank (Option C) — the sinking fund method surrenders more than $125,000 in opportunity cost. (Can you find any opportunities with a better return than 3%?)

That is like stepping over a hundred-dollar bill to pick up a nickel.

With the sinking fund, future cash flows do one thing only: restore the savings account. Yes, each dollar added earns interest — but only for a short time before it is spent again.

How IBC Financing Does Multiple Jobs at Once

By financing a purchase through your own banking system, each future dollar works on multiple levels simultaneously:

- Pays down the loan — reducing principal and accrued interest to the insurance company.

- Restores available capital — each payment reduces the loan balance and increases your Net Cash Value.

- Maintains unbroken compound growth — the policy’s full cash value continues growing throughout the loan period. The loan does not interrupt the growth of the underlying policy.

Compare this to the alternatives:

- Option A (sinking fund): each dollar only increases the savings balance.

- Option B (bank loan): each dollar only decreases the loan balance.

Only IBC financing does both at once — while also maintaining the compounding that the sinking fund permanently sacrifices.

Death Benefit: The Sinking Fund Is Always Replenished

There is one more distinction that conventional finance advice rarely addresses.

Every dollar in your IBC policy purchases death benefit protection for your beneficiaries. If you die before a policy loan is repaid, the loan balance is subtracted from the death benefit — and the remaining death benefit is paid to your beneficiaries. Every loan is guaranteed to be paid off, even if you die (what Nelson Nash called “graduating”) before repayment is complete.

The death benefit (future value) is necessarily greater than the cash value (present value). Your beneficiaries receive not just a replenished “savings account” — they receive significantly more.

Ask yourself:

- Does your savings account provide a death benefit?

- How much does your family receive from your sinking fund if you die?

- If you die, is it restored — let alone restored multiple times over?

The sinking fund is a discipline. IBC is a system — one that works whether you’re here to manage it or not.

Ready to Take Control?

If you’re ready to take control of the banking function (storage, movement, and repayment of money) — or just want to learn more — book a free 30-minute call with an advisor today.

Semper Reformanda.