The Power of Compounding Interest

By

/ Published:

/ Updated:

/ Read Time:

In Brief:

Compound interest is the most powerful force in personal finance — and banks are using it against you. Every mortgage, car loan, and credit card is engineered to maximize the interest you pay while minimizing your awareness of it. The Infinite Banking Concept (IBC) is how you reclaim that power and put unbroken compounding interest to work for your family instead.

In This Article

- What compound interest actually is — and why Einstein (may have) called it the eighth wonder of the world

- How the Truth in Lending Act protects banks, not borrowers

- Why APR is the wrong number to watch — and what to watch instead

- The true cost of your mortgage, illustrated with real numbers

- How 0% financing works — and who it actually benefits

- Nelson Nash’s 34-cent analysis and what it means for your family

- How IBC recaptures the banking function and reverses the flow

“The Eighth Wonder of the World”

There is a quote often attributed to Albert Einstein: “Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” The quote appears in several variations — “the most powerful thing in the universe,” “the greatest invention in human history” — and no one has ever located it in Einstein’s actual writings. Apocryphal or not, the sentiment is exactly right.

Compound interest is interest calculated not just on the original principal, but on all previously accumulated interest as well. Each period’s interest becomes part of the base for the next period’s calculation. Over time, this compounding effect becomes exponential — which is precisely why it is so powerful, and so dangerous depending on which side of it you’re on.

Banks are on one side. Most families are on the other.

The Law That Protects Banks

There are no federal usury laws in the United States. There is no federal maximum interest rate for consumer debt. The exception is the Military Lending Act, which established a cap of 36% APR for active-duty service members — a ceiling so high it would have been considered criminal in prior generations.

Interest rate caps exist at the state level, ranging from 5–15% for undocumented loans. Most states impose no limit on loans made in writing, operating on the assumption that a borrower who signed a contract understood it. When limits do exist, they frequently exempt credit cards — and when they apply to credit cards, they often apply only to banks headquartered in that state.

In 1968, Congress passed the Truth in Lending Act to standardize loan disclosures and protect consumers from predatory lending. The law did standardize the information presented — but it also focused the borrower’s attention on one number: the APR.

That was not an accident. The banking industry lobbied for the Truth in Lending Act. A single percentage point in the single digits sounds reasonable. The total volume of interest paid over 30 years does not. The law ensures you see the former and sign before you’ve fully reckoned with the latter.

APR Is Not the Whole Truth

A 5.3% APR on a 30-year mortgage sounds modest. Mid-single digits. Reasonable. Responsible, even.

Now look at it another way.

A $200,000 mortgage at 5.3% APR over 30 years carries a monthly payment of approximately $1,110. Total payments over the life of the loan: roughly $400,000 for a $200,000 house. You pay 100% of the purchase price again in interest.

Commercial lenders often don’t quote APR to business clients. They negotiate a total volume of interest — a “time price differential” — and expect the borrower to calculate the effective rate himself if he cares about it. The government apparently believes business owners are capable of that math and the rest of us require protection. What we actually received was a disclosure that made a very expensive loan look like a bargain.

Which number matters more to your family’s financial future — 5.3% rate of interest or $200,000 volume of interest?

The Mortgage You’ll Never Pay Off

The amortization schedule is the part of your mortgage disclosure that lenders don’t highlight. In the early years of a standard amortizing mortgage, nearly all of your payment goes to interest — not principal.

At the start of a 30-year, 5.3% mortgage on $200,000, roughly 80% of each payment is interest. That ratio improves slowly over time. But most American families don’t hold a mortgage for 30 years. After 5 years, 76% of each payment is still going to interest.

Military families face this even more acutely. A permanent change of station (PCS) every two to three years means buying and selling homes repeatedly — often in the first years of a mortgage when the interest-to-principal ratio is most punishing. After three years of payments on this mortgage, $40,000 in mortgage payments have only reduced the loan balance approximately $191,000! More than three-quarters of every dollar paid went to interest.

For the average American family that moves every few years, the situation is similar. Equity builds slowly. Interest flows out steadily. The bank collects; the borrower starts over with each move.

This is not accidental. It is the design.

0% Financing: Who Gets the Deal?

Consider the auto dealer offering 0% financing. There is no such thing as a free loan.

Auto manufacturers operate captive finance subsidiaries — Ford Motor Credit, GM Financial, Toyota Financial Services — that are among their most profitable divisions, frequently generating higher profit margins than the vehicles themselves. When a dealer offers 0% financing, the interest cost doesn’t disappear. It is built into the price of the vehicle.

You aren’t getting a lower rate. You’re paying the full interest cost upfront in the purchase price while simultaneously losing the option to pay off early and reduce total interest paid. What looks like a gift is a restructured extraction.

34 Cents of Every Dollar

In Becoming Your Own Banker, Nelson Nash offers an analysis that stops most readers cold: for most Americans, approximately 34% of every dollar spent goes to finance charges — directly or indirectly. This is Nash’s own analysis, not a federal statistic, but the logic is straightforward. Interest is embedded in everything: your mortgage, your car payment, your credit card balance, and the prices of goods sold by businesses that also finance their operations through debt.

When you don’t control the banking function (storage, movement, and repayment of capital) in your own financial life, someone else does — and they profit from it.

The question Nash forces is simply this: what would it mean to recapture even a portion of that 34 cents?

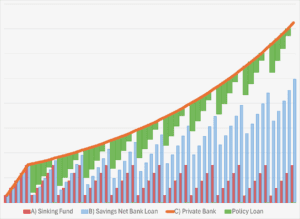

Putting Compounding to Work for You

IBC is the process of establishing a specially designed whole life insurance policy that functions as your own private banking system. Instead of paying interest to a commercial bank and watching that money compound in their favor, you pay yourself, and unbroken compounding interest works on your capital continuously — even while you use it.

If you were able to finance it yourself using an IBC policy, making the same monthly payments you would have made to a mortgage lender, you would reduce principal faster and retain the interest that would otherwise flow out. Over 60 months, that difference compounds.

Over a lifetime, it builds a family economy — liquid, guaranteed, insured, and under your control.

This is what Reformed Finance means by biblical stewardship: not just giving and saving, but understanding who holds the banking function in your household and deliberately taking it back.

If you’re ready to put the power of compounding to work for you or just want to learn more, click to book a free call with us today.

Semper Reformanda