Is TradFi really traditional?

The History of 401(k)s, Roth IRAs, and Conventional Finance

By

/ Published:

/ Updated:

/ Read Time:

In Brief:

“Traditional Finance” is not traditional. The 401(k) was created in 1978. The Roth IRA in 1997. The financial instruments at the center of conventional retirement planning are barely one generation old — and their rise was not organic. It was engineered. What most people call “traditional” is more accurately called conventional — conforming to established practice, not passed down through generations. There is an older, more genuinely traditional way to manage capital, save for large expenses, and plan for the future. That is what this article is about.

In This Article

- Why the term “Traditional Finance” is misleading

- A timeline showing just how new these financial instruments actually are

- Why the shift from life insurance and pensions to 401(k)s happened — and who benefited

- What you actually own (and don’t own) inside a 401(k) or Roth IRA

- The real numbers behind stock market returns

- What truly traditional finance looks like

What Is TradFi — and Why Does the Name Matter?

The term “Traditional Finance” — or TradFi — gets thrown around to describe the government-approved, financial-industrial-complex-recommended approach to managing personal finances: contribute to your 401(k) up to the employer match, max out your Roth IRA, buy term life insurance and invest the difference. This will be validated by Monte Carlo simulations and proprietary software producing a “customized” financial plan that looks exactly like everyone else’s.

The word tradition gives this approach an air of legitimacy and age it does not deserve. It implies this is the way things have always been done — passed down through generations, tested by time. That is not only an appeal to tradition fallacy (arguing something is best because it is traditional), it is based on a false premise.

This is not the traditional way. It is barely one generation old.

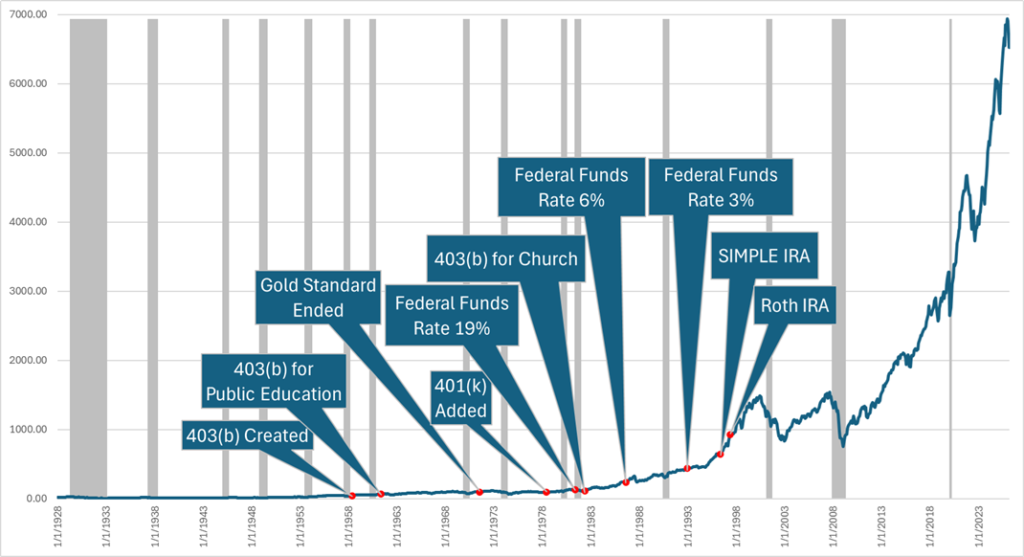

The Timeline: How New Is “Traditional” Finance?

Consider when these instruments were actually created:

- 1997 — Taxpayer Relief Act: Roth IRAs created

- 1996 — Small Business Job Protection Act: SIMPLE IRA created

- 1982 — Revenue Act: IRC Section 403(b) expanded to church employees

- 1978 — Revenue Act: SEP IRA created; IRC Section 401(k) added to the tax code

- 1961 — Revenue Act: IRC Section 403(b) expanded to public education employees

- 1958 — Revenue Act: IRC Section 403(b) added for certain non-profit employees

The oldest instrument on this list is barely 65 years old. The flagship of conventional retirement planning — the 401(k) — is 47 years old. The Roth IRA is 29.

This was not passed down to us by our grandparents. Our grandparents didn’t have it.

What Did People Use Before 401(k)s and Roth IRAs?

Prior to 1958, passive income in retirement came primarily from:

- Pensions — defined benefit plans that guaranteed income for life

- Cash value life insurance policies and annuities — products offered by life insurance companies that accumulated capital over time

- Personal savings accounts and CDs

- Stocks and mutual funds — used, but as the top of the financial pyramid, not the base

The inversion is striking. What was once the speculative peak of a sound financial plan has become the foundation. What was once the foundation has been systematically displaced.

Why Did the Shift Happen?

The transition from life insurance and pensions to 401(k)s was not organic. It requires some background to understand.

The stock market exists to allocate capital. Capitalists want to allocate capital for economic growth. Mercantilists want to allocate capital for personal gain. Our government and financial sector have been dominated by mercantilist interests for well over 100 years — and much of what is blamed on capitalism is more accurately attributed to mercantilism.

Stock prices are driven by supply and demand. High demand for a company’s shares drives the price up, regardless of underlying asset value. This is why a company with $1 million in assets can be valued at $100 million on the market — and why when that overvaluation corrects, executives who sold early profit while ordinary investors, largely through mutual funds, absorb the loss.

In every stock transaction there is a buyer and a seller. Both believe their decision is the more profitable one. The seller would not sell if he believed the price would continue rising substantially. The buyer would not purchase if he believed the shares would lose most of their value.

The Interest Rate Connection

The 401(k) was created in 1978 but wasn’t widely used until the early-to-mid 1980s. In 1981, interest rates peaked at approximately 20%. Americans simply did not have surplus capital to contribute to retirement plans.

Then rates began dropping — falling to roughly 6% by the mid-1980s. This left more money in the average American’s pocket. Newly available capital appeared, and as Nelson Nash noted in Becoming Your Own Banker, wherever capital is accumulated, someone will try to capture it.

Large investment firms began advertising their mutual funds aggressively and started offering 401(k) management to corporations as an employee benefit. The arrangement looked like a benefit to employees. But the companies were the actual clients of the investment firms — and the employees were the funding source. The company benefited too: employee 401(k) contributions could be invested back into company stock, purchased directly by the fund.

This combination — newly available capital, employer pressure toward defined contribution over defined benefit plans, aggressive mutual fund advertising, and government tax-advantaged status — sharply increased demand for stocks. Stock prices rose dramatically. The Austrian Business Cycle boom played out precisely as it would be predicted, followed by the inevitable bust: the Dot-Com Bubble in 2000.

What You Actually Own in a 401(k) or Roth IRA

Most investors assume that when they buy a stock, bond, or ETF in a brokerage account, they become the legal owner of that security. That assumption is wrong in the way that matters most.

In the modern U.S. securities system, the registered owner of the shares in your brokerage account is typically not you — and often not even your brokerage firm. It is Cede & Co., the nominee entity of the Depository Trust Company (DTC), a privately owned institution controlled by the largest U.S. banks and broker-dealers. You are a “beneficial owner” credited on your broker’s books — multiple steps removed from legal title and direct control (McPherrin, 2026).

As former SEC Director Erik Sirri confirmed, shares are held in “fungible bulk — there are no specific shares directly owned by the underlying beneficial owner.” Investors acquire a right to sue a broker — but they do not own specific shares (Jett, 2011, p. 378).

The legal framework governing this arrangement — Article 8 of the Uniform Commercial Code — makes the consequences explicit: under certain conditions, a broker’s secured creditor gains legal priority over customer assets. History has confirmed this in practice. When Lehman Brothers collapsed in 2008, JPMorgan asserted secured claims over customer securities Lehman had pledged as collateral, freezing customer property inside the bankruptcy estate for nearly five years. MF Global and Sentinel Management Group followed the same pattern (McPherrin, 2026).

Under the modern regime, what most customers hold is not a direct ownership interest in a specific security — it is a contractual claim defined by the intermediary system, with priority rules that put banks first during a crisis.

Giving up control of your capital to institutions that hold it in fungible bulk, and hoping for a favorable outcome, is not stewardship. It is speculation dressed in the language of responsibility.

The Real Numbers Behind Stock Market Returns

The performance numbers cited to promote conventional investing deserve scrutiny:

- From 1994–2016, global stocks produced an average return of 7.3%

- Remove the top 10% of performing stocks — returns drop to 2.9%

- Remove the top 25% — average return falls to -5.2%

- From 1990–2009, just 1.3% of stocks were responsible for producing all of the gain above treasury bills

The conventional financial plan bets the average investor’s retirement on outcomes driven almost entirely by a small fraction of exceptional performers — while the investor has no ability to identify those performers in advance, no control over the capital, and no specific ownership of what they think they hold.

What Truly Traditional Finance Looks Like

Taking control of the banking function (storage, movement, and repayment) in your own life is not a new idea. It is the older idea.

Using a properly structured, dividend-paying whole life insurance policy to save for large expenses, fund emergencies, and build toward passive income may not be conventional today — but it is traditional. It is what families did before 1958. It is what the financial industrial complex displaced. And it is what Reformed Finance exists to help families reclaim.

As Nelson Nash said: “When you know what is going on, you’ll know what to do.”

This is what Reformed Finance is about — not a new gimmick or a modern innovation, but a return to a more traditional, more biblical approach to managing the resources God has entrusted to us.

Reform your banking, reform your life.

Semper Reformanda

If you’re ready to break out of the conventional financial advice, or just want to learn more, click to book a free call today.

References

McPherrin, J. (2026, February 4). You don’t own your stocks the way you think you do. ZeroHedge. https://www.zerohedge.com/markets/you-dont-own-your-stocks-way-you-think-you-do

Jett, Wayne (2011). The Fruits of Graft, Los Angeles, CA: Launfal Press